How to risk it all (while bluffing your way through it) with Maria Konnikova, author of the new book “The Biggest Bluff.”

At HerMoney, we love behavioral finance — specifically, learning what we do with our money, and how our emotions play into our decisions. Whether we’re motivated by fear, or maybe a desire for control, or even love — those deep-rooted “whys” that we all have can change everything.

And wrapped up in all these decisions is risk. How much risk we take in the stock market, the risk we take when we buy a property, or the risk of going out on a limb to start our own business. If you listen to some of the most successful investors and business people in the world, they’ll tell you that at some point — maybe at many points — they had to roll the dice, and do a little bluffing to get where they are today.

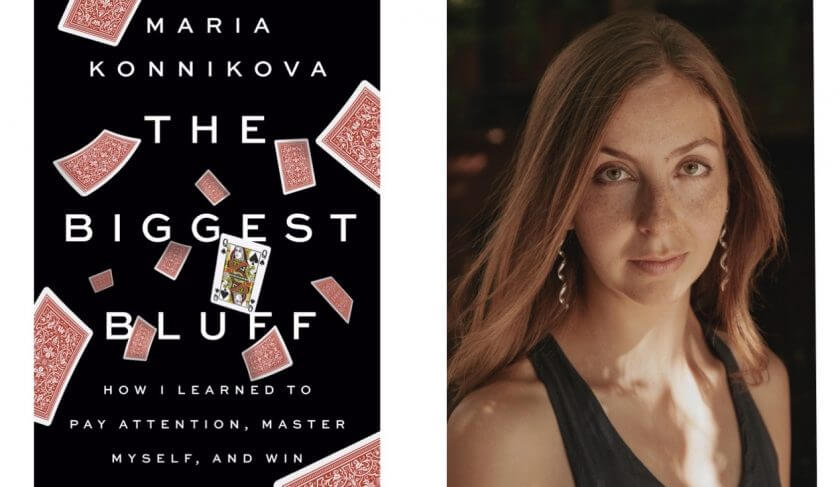

This week we’re diving in feet first to talk about risk and luck with one of the world’s leading authorities on the topic, Maria Konnikova. Maria is the author of the new book, “The Biggest Bluff: How I Learned To Pay Attention, Master Myself, And Win,” and during her time writing and researching this book, she actually became an international poker champion and the winner of over $300,000 in tournament earnings. Maria is also the author of two other books you may have heard of, including “Mastermind,” and “The Confidence Game,” and she has her PhD in psychology from Columbia University.

Listen in as Maria tells Jean how she ended up in the world of poker, and why she decided to study risky decision-making under uncertain conditions for her PhD. Amazingly, she’d never played a hand of poker in her life until she started researching “The Biggest Bluff.”

Maria also talks about the role that luck plays in life, and shares her personal philosophies on luck as it relates to fate, and how all of it ties back into what we can and can’t control. Maria also discusses what she’s observed about good investors — they are skilled at the “illusion of control,” meaning that they don’t take as much negative feedback from their environment. In other words, they’re able to tune out the noise and focus on the long game.

“Poker, just like life, is a game of informational advantages. If I have more information than you, that’s great. But how do I get that? How do I actually acquire as much information as I can in order to make my decision? How do I make it, knowing that there is no such thing as 100% certainty?” Maria asks.

She also discusses why our emotions are so critical to any decision making process, and how they guide how we analyze information.

“It’s your decision process, it’s your logic, it’s the information you’re taking in, the information you’re using, how you’re analyzing that information, and it’s also your emotions. That’s so crucial in any kind of decision making. It’s also taking control of your mental state. How are you interpreting things? How are you reacting? Are you letting emotions into your decision process or not? Are you accounting for the fact that you’re tired, for the fact that you’re hungry, for all of these different things? That is the stuff that you can control. What you can’t control is the cards, the next card, the outcome, that’s just noise.”

Lastly, Maria breaks down the art of bluffing for all of us and tells us how to bluff, and how to observe someone who may be bluffing us, and the moves and decisions they might make. Perhaps not surprisingly, a lot of these skills helped turn Maria into an expert negotiator, and she shares some important takeaways we can all use in our careers.

In Mailbag, Jean and Kathryn tackle caring for aging parents, target date funds, caring for a significant other financially, and taking a 403b loan. In Thrive, should you take a gap year if your college is closed this fall

This podcast is proudly supported by Edelman Financial Engines. Let our modern wealth management advice raise your financial potential. Get the full story at EdelmanFinancialEngines.com. Sponsored by Edelman Financial Engines – Modern wealth planning. All advisory services offered through Financial Engines Advisors L.L.C. (FEA), a federally registered investment advisor. Results are not guaranteed. AM1969416

Editor’s note: We maintain a strict editorial policy and a judgment-free zone for our community, and we also strive to remain transparent in everything we do. Posts may contain references and links to products from our partners. Learn more about how we make money.

The HerMoney podcast is supported by

![]()

All advisory services offered through Financial Engines Advisors L.L.C. (FEA), a federally registered investment advisor. Results are not guaranteed. AM1969416

Transcript

Maria Konnikova: (00:00)

It’s your decision process. It’s your logic, it’s the information you’re taking in. The information you’re using. How you’re analyzing that information. And it’s also your emotions. That’s so crucial in any kind of decision making. It’s also taking control of your mental state. How are you interpreting things? How are you reacting? Are you letting emotions into your decision process or not? Are you accounting for the fact that you’re tired? To the fact that you’re hungry? For all of these different things? That is the stuff that you can control. What you can’t control is the cards, the next card, the outcome. That’s just noise.

Jean Chatzky: (00:41)

HerMoney is supported by Fidelity Investments. We all have our own financial needs and goals. Investment advice from Fidelity can help you reach yours. Plus they have tools like financial checkups and more to help you make smarter, well-informed decisions every day. Visit Fidelity.com/HerMoney to learn more.

Jean Chatzky: (01:08)

Hey everybody, I’m Jean Chatzky. Thank you so much for joining me today on HerMoney. If you are a regular listener to this show, I suspect you already know that one of my favorite topics to dig into is behavioral finance. I really get into learning why we do what we do with our money and how our emotions play into our decisions. Whether we are motivated by fear or a desire for control, or even love, these deep rooted whys that we all have can change everything. And wrapped up in every single one of these decisions is risk. How much risk we take when we’re in the stock market or buy a property or start a business. If you listen to some of the most successful investors and business people in the world, they will tell you that at some point, maybe at many points, they had to roll the dice and do a little bluffing to get where they are today. And so today, we are going to be talking about risk, about luck, about bluffing with Maria Konnikova, the author of the new book, “The Biggest Bluff: How I Learned to Pay Attention, Master Myself and Win.” During her time writing and researching this book, she became an international poker champion and the winner of over $300,000 in tournament earnings. Maria is also the author of two other books you may have heard of including “Mastermind” and “The Confidence Game” and she has her PhD in psychology from Columbia University. Hey Maria.

Maria Konnikova: (02:53)

Hey Jean. Thank you so much for having me on the show.

Jean Chatzky: (02:56)

Thank you so much for being here. Thanks for digging into this fascinating topic. I’m very, very excited. I think you can probably tell,

Maria Konnikova: (03:06)

Well, I hope I won’t disappoint you.

Jean Chatzky: (03:08)

Can you start by telling us a little bit about you? I mean, you’re in your mid-thirties, but you have quite a resume including an undergrad degree from Harvard, a doctorate from Columbia. How’d you get going and what inspired you to dig into poker?

Maria Konnikova: (03:24)

Absolutely, absolutely. So my background, as far as academics go as an undergrad, I studied decision making from two perspectives, from the psychological perspective and also from political science. I was really interested in leadership decision making and international relations and how people in high levels thought. And I also studied creative writing and fiction because I knew that I wanted to write. And I remember falling in love with the ability to write about the human mind when I first read Oliver Sacks’s “The Man Who Mistook His Wife for a Hat.” I just thought, wow, I want to do that one day. And so when I left undergrad, I did try to write, but it was really hard and I didn’t have any money of my own, no financial safety net and writing doesn’t pay very well, especially if you’re a nobody. So, I did some other things and then decided to go back to graduate school to study psychology and had a chance to study with just one of the absolute legends of the psychology world. My advisor was Walter Mischel, who people might know as “the marshmallow guy.” The guy who designed those famous marshmallow studies that show that the amount of time you could spend waiting for a marshmallow as a child, could really correlate well with how well able you were to delay gratification at later points in life. And that that in turn led to better academic outcomes, better financial outcomes, better health outcomes. Just all sorts of positive things. And I had a wonderful experience working with him and we specifically worked on decision making under conditions of risk and uncertainty. And I actually had people play stock market games. That’s what I did my dissertation on.

Jean Chatzky: (05:07)

Wow.

Maria Konnikova: (05:07)

To see how they reacted and whether or not they could make good decisions under hot emotional conditions or not. And what it would take to get them off balance. And one of the things that we found was that really smart people and really good investors were very prone to something called the illusion of control, which means you put them in a stochastic environment, in an environment with a lot of randomness and noise, with a lot of uncertainty, and they think that they control much more than they actually are. And they don’t take as much negative feedback from the environment. People who didn’t know anything about investing, they were like, when our environment changed and the good stocks became bad stocks, they changed their strategy really quickly. They thought, ut oh, I’m losing money. Better try to figure this out. But the good investors are like, ah, no, this is just noise. I’m good. I’m in control. This is great. I’m just going to keep doing what I’m doing. And they’d lose a lot more money in the end. And this really struck me and stuck with me because I thought, wow, really smart people can think that they control things that they don’t. And then they take credit for things that they shouldn’t be taking credit for quite often. And it was a problem that had really stayed in my mind, but not one that I could really see a way to solving within psychology. And after Columbia, I became a full-time writer, as you said, wrote two books “Mastermind” and “The Confidence Game.” And when it came time to figure out what I was going to do after “The Confidence Game”, this question of luck came back to me. And a lot of things happened in my life. That was a very personal decision at the time to write about luck. I got very sick. My grandmother died. People lost their jobs. Just a lot of things going wrong. And it made me realize, you know what? Sure we can take credit for a lot of our success, but actually we also have to get so insanely lucky to get to where we are. And if the luck stops going in our direction, then we’re in trouble if we don’t know how to deal with that. And I wanted to explore that. And I started reading about game theory because that’s one of the ways that you can approach chance. And read for the first time, I had somehow never read it before, the foundational text of game theory, “The Theory of Games”. One of the authors as John Von Neumann, and it ends up that Von Neumann was a poker player. And that poker was the inspiration for game theory. And what he said was, poker is the perfect game if you actually want to answer these questions, tackle this issue of skill versus chance, because it’s a game of incomplete information. It’s a game where there’s information that I have that you don’t have, but there’s also information that you have that I don’t have. And I need to try to figure out how much you know, and you need to try to figure out how much I know and we’re playing each other as much as we’re playing the cards and the odds. And it’s a game of people. It’s a game of intention. It’s a game of reaction. And so he said, this is the mathematical tinged with the human. That’s what life is. Good decision making in life isn’t just pure math. That’s impossible. You can’t have an algorithm that will tell you, here’s what you’re supposed to do now, simply because there’s too much uncertainty. There are too many unknowns and there’s the human factor. But what if we can figure out a way to put the two together? And so he thought, wow, if I solve no-limit hold’em, which is the variant that I ended up playing and what he played, I’ll have this key to solving strategic decision making. No-limit hold’em still hasn’t been solved. It’s the gold standard of AI research. But this really intrigued me and I thought, wow, what is this poker thing? I’d never been a poker player.

Jean Chatzky: (08:44)

Well, that was unbelievable to me that you’d never played a hand of poker in your life.

Maria Konnikova: (08:50)

Yeah, it was just never something that interested me. I grew up in a household where there were lots of books and really no games. I don’t even think we had a card deck. It was just not something we did as a family. And so I just didn’t have much of an interest in it. I didn’t not like poker. I just didn’t know anything about it. I didn’t know what it was. And it was fascinating to me to see that one of the greatest minds of the 20th century was fascinated by the game. And so I decided I’m going to learn this. I want to find someone who can teach me how to play, someone really, really good. And originally it was supposed to be just one year and using poker as a laboratory for going through a lot of these psychological ideas. And it ends up that I became really good and became an international champion and became a professional poker player. And that was not something I could have ever predicted was going to happen. So it turned into a little bit more than a year.

Jean Chatzky: (09:45)

Explain to me where luck fits into that. The fact that you did become really, really good and won a lot of money and went on the championship circuit and got a sponsor from one of the biggest brands in the game. Was there an element of luck in that, or is that a hundred percent skill?

Maria Konnikova: (10:07)

I don’t think anything is a hundred percent skill. I think it’s such a fallacy to think that we can really take credit for any one thing. And so there was a ton of luck in that. I always say that poker is a game of skill, but in the short term, in one tournament, in one hand, luck can really be the guiding force because anyone can get lucky and be dealt the best hand one time, right? Or over one tournament. But over dozens of times, hundreds of times, thousands of times, that’s just simply not going to happen. Variance is going to even out and the skilled player is going to win. That said, in order to win a tournament, you need to be very good, but you also need to get very lucky. And my entire trajectory in poker wouldn’t have looked the way it did had I not won this major title, the PCA National Championship in 2018. And if you think about it, sure, I played well. But I also had to get very lucky to get to that final table. I had to win in a few key situations. So, I had to make good decisions, but I also had to have luck be on my side. And not be on the wrong side of variances. Oftentimes, you make your decision as a 75% favorite and all of a sudden you’re out because the 25% happened. So, you really need your luck to hold. And I’ve thought about this many times, what if I hadn’t won? What if I had just come in second? I don’t think I would have gotten sponsored. I don’t think anyone would’ve cared because no one really cares about second place finishers that much. They care about the champion. It’s a very different story. So there was a huge element of luck there because I could have gotten just as good as I did and never have won a major tournament. There’s lots of wonderful players who’ve never come in first because at the end of the day, luck just doesn’t go in their direction. And I think it’s so important realize that – that you can make really good decisions and your process might be correct, but there’s variance and poker shows you that because the cards are something that you do not control. The next card from the deck, that can change everything completely. As long as you made the right decision, as long as your thought process was clear, as long as you got your money in as a favorite, you need to keep doing that over and over and over even if you lose. You have to divorce yourself from the outcome. In this particular case, the outcome went in my direction and sure there was skill, but there was also a lot of luck.

Jean Chatzky: (12:29)

You raised the issue of control. And I know that that is a very big part of the skill in good decision making. Even in these times of coronavirus, as I’ve been talking to people about their money, I’ve really fallen back on talking about how important it is to control the things that we can control in these uncontrollable environments. Tell me how you think about control in the context of decision making.

Maria Konnikova: (13:04)

Absolutely. I think it’s so important to learn to separate the things that you can actually do something about from the things that you can’t. And to focus on the former. And just learn to let go of the things you can’t control, because it will really screw with you psychologically and emotionally if you keep focusing on the outcome and the outcome is out of your hands. And so what poker teaches you is a very stoic philosophy to be perfectly honest. It’s a philosophy of play as well as you can. What can I control? Okay, well, I can’t control the cards I’m dealt. I can’t control the cards that anyone else is dealt. I can’t control the cards that are coming from the deck. All of that is totally out of my hands. So, I shouldn’t worry about it. What I should be focused on is how do I play? How am I actually playing my hand? What am I thinking? What’s going into my decision? How am I reacting? What am I doing in response to other people? Am I observing? Am I taking in as much information as I can? Or am I being lazy? Because poker, just like life, is a game of informational advantages. If I have more information than you, that’s great. How do I get that? How do I actually acquire as much information as I can in order to make my decision? How do I make it knowing that there is no such thing as 100% certainty. That I should be grateful if I get my money in as a 65% favorite. That that’s okay because those are wonderful odds. How do I learn to think in those terms and just let go of the other things. So it’s your decision process. It’s your logic. It’s the information you’re taking in, the information you’re using, how you’re analyzing that information. And it’s also your emotions. That’s so crucial in any kind of decision making. It’s also taking control of your mental state. How are you interpreting things? How are you reacting? Are you letting emotions into your decision process or not? Are you accounting for the fact that you’re tired, for the fact that you’re hungry, for all of these different things? That is the stuff that you can control? What you can’t control is the cards, the next card, the outcome. That’s just noise and you shouldn’t worry about it. One of the things my coach taught me very early on is, don’t worry about how the hand actually ends. You don’t care whether you win or lose, you care about your decision process. And to me, at the beginning, that didn’t make much sense. I thought, well, of course I care if I win or lose. But what he was trying to do was get me to focus on the right things because you can’t control whether you win or lose. What you can control is, did I make the right decision?

Jean Chatzky: (15:39)

So interesting. And I want to dig further into this concept of getting the right information, but also telegraphing the right information, bluffing in other words. But before we do that, let me remind everybody, HerMoney is proudly sponsored by Fidelity Investments. Whether you are looking for a turn-key way to save and invest, or you need to tap the support of an experienced pro for a more complicated financial picture, Fidelity is there to help you meet your goals. In addition to investment advice, Fidelity has online tools like financial checkups that can help you make smarter, more informed decisions every day. Visit Fidelity.com/HerMoney to learn more. And that’s exactly what we’re talking about – making more informed decisions. Decisions where we have more information than the other person. We’re talking with Maria Konnikova author of the new book, “The Biggest Bluff: How I Learned to Pay Attention, Master Myself and Win.” I’d like to talk about bluffing, but I want to make sure we talk about bluffing in the context of being women. And how it can hurt us, how it can help us, how we can be better at it than the other guy.

Maria Konnikova: (16:59)

Absolutely. And I think that that’s crucial. And that’s one of the main things that I learned in poker because I came into poker as me. And me is female. And poker is 97% male. Just think about that number for a second. How many areas? I don’t know, a single other area that’s actually 97% male and only 3% of the professionals are females. So, you can go for days and not see another woman. And so you really have to understand that people’s perceptions of you are very different. The first thing they notice is that you’re female, because it stands out.

Jean Chatzky: (17:37)

Uh huh.

Maria Konnikova: (17:37)

That’s actually your defining characteristic. And I realized that people would see me as a female first and as a poker player second. And, at first, it actually really affected me negatively. And I made poor decisions because I realized that I had a lot of socialization layers that I had to work my way through. I had a lot of psychological hangups. I couldn’t bluff enough. I wasn’t aggressive enough because I didn’t want people to dislike me. I wanted them to think I was nice.

Jean Chatzky: (18:07)

Oh boy.

Maria Konnikova: (18:08)

And that’s terrible. Exactly. That’s an awful way of playing. And when I realized that, it was not a pleasant realization. I think of myself as a strong woman. And nope. It ends up that I have these hang-ups that came out at the poker table and all of a sudden, I thought, wow, I have to deal with this. This is a problem. And obviously if it’s happening in poker, it’s happening everywhere else. And so, I try to figure out, okay, first, how do I overcome this? But also how do I use the fact that people are underestimating me? How do I use that to my advantage? And once I realized that I could flip the tables, it made me much better able to not just bluff more, but to bluff well, to bluff intelligently, to figure out how do I use people’s perceptions of me to run bluffs that are actually going to be successful. So, I’ll give you a few examples.

Jean Chatzky: (19:03)

Sure.

Maria Konnikova: (19:03)

I’ve encountered men who just don’t think women are capable of bluffing. You know, she’s just straight forward. She’s a girl. She doesn’t have the balls to pull it off. And so, when I encounter someone like that, what the best strategy is? You bluff them like crazy because they’ll fold because they think, wow, she must be getting really good cards, because she can’t lie. She can’t bluff. She’s not good enough to bluff. So that’s what you do there. Then there are the men who would rather die than be caught folding to a bluff from a girl. To them, that’s just the ultimate threat to their ego. So, they will never fold to me. And for them, I never bluff them. My bluffing frequency goes down to zero. And instead, I bet like crazy when I have any where close to a decent hand. A hand that I might check against someone else, because it’s really not good enough to bet multiple times, because it’s good, but it’s not amazing, I will bet it so hard because I know that he’s going to call me with nothing, because he’s so afraid of being made to look weak and folding to a girl. So I can get his money that way.

Jean Chatzky: (20:11)

How do you know who he is on the other side of the table?

Maria Konnikova: (20:15)

That is the first thing that we were talking about. Observing, paying attention and actually taking in information. So, what I do at the beginning, is I end up not even playing oftentimes for the first hour or so when I’m at the table. I’ll just play a few hands and I’ll observe. I’ll look at how people are responding to me. I’ll look at how they’re talking about me or to me. I’ll just look at their body language and I’ll observe. I’ll look at how they’re playing and then I’ll play a few hands. See how they play against me. And over time, I can start building up a picture of who they think I am and what they think a woman is like. Because you see all of these hang-ups at the poker table. And by the way, this is true of me too. I also have stereotypes about certain types of people. I’ve made horrible mistakes when I’ve been seated at a table and all of a sudden, a guy with tattoos and these huge biceps sits down, and his neck is bulging and I’m thinking, oh wow, he’s going to be an aggressive maniac bully. I’m not going to let him push me around. And then, I end up losing all of my chips because it turns out he’s a very conservative player who is not a bully at all. And so, it was an oops moment of complete misperception. So, I do it, too. I don’t want it to seem like, oh, these guys are making all these mistakes, but I don’t. So, everyone does it. But the goal is to try not to do that. And instead to be one step smarter and to observe how they’re acting and how they’re actually playing hands. That’s the information that’s valuable, not how they look.

Jean Chatzky: (21:47)

Many of us don’t play poker every day. Some of us don’t play poker at all. But I think there is so much in what you’re saying that we can use as investors. We can use as shoppers. We can use when we are negotiating for our next raise. Can you synthesize it a little bit?

Maria Konnikova: (22:06)

Sure. I mean, I think that we need to be aware that nobody knows what cards we hold. That’s such freeing information and, it seems really trite, but it’s really hard to internalize. It’s really hard not to think, oh, they see through me. They know that I have bad cards. They know that this is a bluff. Well, they only know if you show them. And so, I’ve actually become much better at negotiating. By the way, I hate negotiating. It’s really hard for me. It doesn’t come naturally at all. And I wish I never had to do it. That said, poker has made me much better at it because it’s made me realize, no one knows what you really hold. All they know is what you’re projecting. And so I’ve tried to take a page from that and to project more confidence than I’m feeling. Project a position of a little bit more strength than I might necessarily feel. And that’s really helped. And what’s also helped is being smarter about my strategy. There’s one negotiation that I write about in the book that I counted as a personal triumph. And it was me being able to negotiate a higher per word rate than I was able to do before from this publication. And it was me just playing smarter poker. I realized that they wanted something from me and that I could basically just say, you know what? I don’t want to play right now, but I’m not going to step away from the table. So I didn’t raise them. I didn’t say I want more money. I said, you know what? I’m really busy right now. I can’t take anything else on. I left the door open for them to come back, which they did. They said, well, what if we pay you a little bit more? And, you know, old me would have definitely jumped at that and said, yes, please. And new me just said, you know what? I really appreciate that. But it just doesn’t make sense for me right now, unless I get paid more than I am at my home magazine. And then they came back with a per word rate that I’d never thought that they would be capable of and I accepted. And I never would have been able to negotiate like that in the past.

Jean Chatzky: (24:07)

Maria Konnikova, I can’t wait to see the movie. This book is fabulous. It’s called “The Biggest Bluff: How I Learned to Pay Attention, Master Myself and Win.” Where can we learn more about you?

Maria Konnikova: (24:24)

You can learn about me either at my website, which is mariakonnikova.com. But I admit, I don’t update that very often. Or social media, mostly Twitter, which is @mkonnikova and Instagram where I’m grlnamedMaria, but girl without the eye. Just GRL, because somebody had already grabbed the girlnamedmaria with an I handled before I had a chance to do it myself.

Jean Chatzky: (24:45)

Thank you so much for being here with us today.

Maria Konnikova: (24:48)

Thank you so much for having me, Jean. It’s been a pleasure.

Jean Chatzky: (24:51)

For me too. And we will be right back with Kathryn and your mailbag.

Jean Chatzky: (25:03)

And HerMoney’s Kathryn Tuggle is with me now. That was so much fun.

Kathryn Tuggle: (25:08)

Oh my gosh. I loved her. I’m going to go out and get the book right now.

Jean Chatzky: (25:12)

Yeah. I was casting the movie in my head as she was talking. Because, Molly’s Game. Have you seen Molly’s Game?

Kathryn Tuggle: (25:19)

I have, yeah.

Jean Chatzky: (25:20)

It’s one of those movies that I will watch again and again and again and again. And she runs a poker game. But she doesn’t play poker. So, I’m very excited to see what happens with this. My money is, not that I’m betting, but she got me in a betting mood, I think Anna Kendrick. What do you think?

Kathryn Tuggle: (25:37)

I can see that? I don’t know if Anna Kendrick is badass enough. Can I say that on this podcast? Maybe not.

Jean Chatzky: (25:43)

You can say that. You can absolutely say that. Who would you cast?

Kathryn Tuggle: (25:49)

Um, I think I might go with Emma Stone because she is cute, but she has an edge.

Jean Chatzky: (25:55)

Oh. See I was looking for the edge and I think Anna Kendrick has one. But, you know, she’s very diminutive. So, maybe, I don’t know, that would either work or not work against the men at the poker table.

Kathryn Tuggle: (26:09)

Yeah. I think you have to be able to own the room.

Jean Chatzky: (26:12)

Yeah, we’ll see.

Kathryn Tuggle: (26:14)

Yeah. Yeah.

Jean Chatzky: (26:15)

It will be a movie before we know it. I am sure.

Kathryn Tuggle: (26:19)

Totally.

Jean Chatzky: (26:19)

Let’s kick off our mailbag.

Kathryn Tuggle: (26:21)

Absolutely. Well, we can start with a little good news from a listener named Linda who wrote to us. Hi Jean and Kathryn. I’ve been listening to the podcast for three months and have almost completed “Women with Money”. After several years of procrastination, but finally motivated and propelled by caffeine and dark chocolate, I decided to look at my investments so I can thoughtfully rebalanced my portfolio in 2020. Like many of your listeners, I glaze over when looking at numbers, but I realized that I had to get a handle on my financial fitness before downshifting into retirement. Thankfully, my situation is not as bad as I thought. Thank you so much for your enthusiastic focus on educating women about money. I look forward to continuing to learn from you, your staff and your guests.

Jean Chatzky: (27:04)

I love that letter. Thank you so much, Linda. Yeah, I think a lot of people right now are digging in and realizing it was bad. It’s now better. It might get a little bit worse again as we go through coronavirus, but not looking is never the right answer. So I’m excited for you and proud of you and happy to have you as part of our community.

Kathryn Tuggle: (27:27)

Absolutely. Having all those answers and all that information can be so empowering.

Jean Chatzky: (27:33)

Uh huh. Exactly. We got to get honest with the numbers for sure.

Kathryn Tuggle: (27:35)

Our first question today is from an anonymous listener. She writes, my husband and I are millennials and dual income, no kids yet. We are 30 and just got into well paying jobs where we’re saving more than 50% of our income and we’re going to pay off our student loans by the end of the year, while also maxing out both of our Roth TSPs retirement plans and contributing to a college savings account and Roth IRAs. We only have a small savings, under $5,000, because we’re trying to take advantage of our current age and income to gain compound interest on long-term priorities. My husband is active duty military and we’re stationed in Japan for the next two years. Our savings is small and we’re prioritizing other accounts because we do not pay for rent or utilities or healthcare or kids as of right now. My husband’s father, who is a divorced functioning alcoholic and smoker with very little money, at the age of 65, just quit his job and moved in to care for his mother and has requested our financial help to keep his home and pay his monthly expenses. The grandmother’s home is a reverse mortgage, so he will not be able to live in her home once she passes. He has poor credit. He bought a home in 2008, so he owes only a little less than his home is worth. And we cannot physically help him due to our location. But also we do not have a secure situation to be able to financially help, unless it’s absolutely necessary. Plus, we don’t fully trust where the father’s money goes. How do we juggle our quest to get debt free, to keep our careers going and start a family while parent care and even grandparent care are also demanding our attention? What should we do?

Jean Chatzky: (29:21)

It is so, so difficult. And I really think that you have to prioritize your own financial situation and that the one line of your story that you need to hold is that you say, right out loud, that you don’t have a secure enough situation to be able to financially help right now, unless it’s absolutely necessary. And you don’t trust where his money is going. I mean, that is the heart of this story. But clearly, because you write, you want to do something. I would look at two things here. The first is that reverse mortgage on the grandmother’s home. Just because there’s a reverse mortgage on the home, doesn’t mean that there’s no equity in the home. It depends on how recently she took out the reverse mortgage and how much of the equity has been used. But many reverse mortgages are structured as lines of credit. And there is some, if not a decent amount, of equity left there. I assume that after the grandmother passes away, your husband’s father will inherit that, whatever is left. That’s an opportunity for him, if there is something there, to get back on his feet financially. So, I would look into that and see what’s available. As far as helping him by giving him additional money, I wouldn’t do it unless I could see that there was a plan in place for how that money would be used, an advisor in place to help keep an eye on the use of that mone and a really, really strict time horizon in terms of how long this support was expected to continue. Your husband’s dad could live a very long time and you don’t want to be in the position of mortgaging your own future and your kids’ own future in order to take care of them. If you can get a financial advisor into sit down, look at your husband’s father’s situation, figure out when is the right time to pull the trigger on social security, as well as any other money he has coming in, and roll that together with any assets that will be inherited from the grandmother and grandfather, hopefully, you can stave off the need to actually start writing checks. But again, it is something that I would be really, really reluctant to do. And that’s a really hard thing to say, Kathryn. You know, when our parents need help, we step in and we help. But it’s a cycle that is very difficult to get out of once you get into it. And if these folks rob their own futures because they’re paying for this man’s future, this irresponsible sounding man’s future, then their own children will have to step up and pay for them.

Kathryn Tuggle: (32:46)

Yeah. I think Rob your own future is such a good way to put it. And when we talk about how these things can snowball, I mean he’s 65. He could be asking for financial support for another 30 years.

Jean Chatzky: (32:59)

Exactly.

Kathryn Tuggle: (33:00)

And that is a slippery slope.

Jean Chatzky: (33:02)

Yeah. So be very, very careful.

Kathryn Tuggle: (33:05)

Yep. Our next question is from Sam, from California. She writes, hi Jean. I first started tuning into your Today Show segments back when I was in college. About a year ago, I was so excited to discover your podcast. And because I grew up watching you, I knew that I could trust your sage advice. Listening to you regularly has empowered me to make my money work harder for me and my life goals. My question is about target date funds. In my twenties, I learned that this was a less intimidating way to ease into investing – similar to a set it and forget it approach. So I opened my first Roth IRA with Vanguard, target date fund 2050, in July, 2015 through a rollover from her previous job. I recently completed another rollover and decided to invest the $38,000 in a more aggressive fund, target date fund 2060. Between these two funds and an additional IRA. I have about $110,000. I just turned 33 years old and now I’m wondering, are target date funds still the best way for me to invest in retirement? Or should I be more active in diversifying my own portfolio now that I’m older, wiser, and more willing to do the research. To be honest, I’m still a little overwhelmed by the thought of that. I should also add that my husband and I recently decided to open up a brokerage account with Fidelity and will contribute up to $20,000 to be more active and conscious investors like purchasing ESG funds and other individual stocks. I’m leaning towards keeping my target date funds the way they are with Vanguard and focusing my energies on the new brokerage account with Fidelity. What do you think?

Jean Chatzky: (34:34)

I think that sounds fine actually. I do. I think reading between the lines of your letter, you are sounding to me like you’re not ready to take your money out of those target date funds. That you know that this is the bulk of your nest egg for retirement, at least right now and you want it to be professionally managed going forward. The one question I have about that $110,000 is the mention of your additional traditional IRA. When you go the target date route, it’s meant to be a one and done solution. And so I just want to make sure that you’re not messing up the asset allocation in those target date funds by putting some of the money somewhere else. I’d like you to take a look at that. But as far as taking a slice of your money and using it to be a more active, more conscious investor, as you put it, that’s very nice turn of phrase. And managing that money yourself, I think that’s terrific. And it’s exactly what we are hearing from other millennials like you. We are hearing that you want to use your money to make the world a better place, to make the world into the world that you want to live in. I am all for that. Kathryn and I were just talking yesterday about programming an additional show on ESG funds and how to put your money where your mouth is in this way. So, you can look forward to that in the next couple of months and good luck.

Kathryn Tuggle: (36:13)

Yeah. Good luck. Our last question is from Lee. She writes, hi Jean. Thank you for your podcast. I’ve listened to every episode since discovering it a couple of months ago. In my twenties, I was married to a man with severe substance abuse issues and spent a decade caring for him. In my thirties, I found the man who I cared for in a different way – financially. I ended that relationship, sold the house I had purchased as he did not contribute as planned, and my finances were unsustainable. So, I finally started taking care of myself and getting my finances in order. My questions. I had taken a 403b loan, and I still owed $24,000. My other debt is also $24,000 on my car. When I started working at my current hospital job, I was in the process of divorce and basically didn’t think about retirement. I’ve been contributing 4%, but my retirement account is way behind at a hundred thousand dollars. My income is about $110,000 annually, and I’m almost 42. Before finding you, I was listening to Dave Ramsey and I was about to stop contributing to my 403b in order to plunk all my money down on my car. But instead I increased my retirement contribution rate to 10%. I’m hoping for some guidance with prioritization. Where do I begin to reach my bigger financial goals. In addition to saving for retirement. I also want to save for a down payment on a small house. Thank you so much for your guidance.

Jean Chatzky: (37:34)

You’re welcome. And I just want to say that I don’t think 42 is such a late start to get going. And you’ve already started. You’re getting there. I got divorced when I was 40 and I felt like I was really starting over at that point. So, I know that it’s possible cause I’m 55 now and I’ve made a lot of headway and I think that you will be able to do the very, very same thing. I’m really glad that you upped your contribution to your 403b rather than putting the money down on your car. Because here’s what I’d like you to do. I want you to take a look at the interest rate that you’re paying on that car. We don’t talk about it very much, but car loans are very, very simple and easy and cheap to refinance and interest rates right now are super low. So, look for a good deal on a used car loan refi. Often credit unions have really, really good deals on this. And use that lower interest rate to your advantage. I’m not exactly sure how old your car is, but you want to make sure that you don’t extend the term of your loan for longer than you think you’re going to want to keep that car. In fact, I wouldn’t extend the term of your loan at all. Look at a 36 month refi or a 24 month refi, whatever lines up with the loan that you have now. And then take the money that you’re saving on that car loan and perhaps put it into a fund for a house or perhaps add it to the money that you’re putting aside for retirement. The other thing I want you to do right now is to just look at where your money is going. $110,000 is a great salary. We’ve all made considerable changes in how we’re spending. Thanks to the fact that we’ve been home a lot more than we’re used to. So just look at whether you have even more money that you can sock into a small separate fund for that down payment on a house or other goals that are coming along the way. It sounds to me like you are really, really moving in the right direction. And I’m so glad to see that.

Kathryn Tuggle: (39:53)

Yeah, definitely. That’s a great salary and 42 is so young. So many more years to save.

Jean Chatzky: (39:59)

So young. So, so young. Absolutely. Kathryn, thanks so much.

Kathryn Tuggle: (40:05)

Thanks Jean.

Jean Chatzky: (40:06)

And in today’s Thrive, should you take a gap year if you’re college is closed this fall? If you’re considering it, it’s important to weigh the pros and cons carefully, especially since deferral rules vary by school. Some have tightened those guidelines in anticipation of more students requesting time off this year. So, if you’re considering it, check your school’s website for its COVID-19 deferral policy, then reach out to the admissions office or registrar with questions about your specific situation. If it’s financially possible for you. It’s a good idea to continue your education by your chosen school’s online courses to avoid slowing your momentum and to stay connected to the academic experience. Keep in mind, a gap year isn’t costless in the sense that you’re pushing graduation out a year. Taking a gap year also means delaying your post-college salary, your ,future seniority in the workplace, and potentially your grad school start date. But if school this fall just isn’t in the cards due to financial concerns or good old-fashioned loathing of online learning, a gap year can be an incredible opportunity to give back on a local or national scale. If you’re drawn to volunteering, think critically about the problem you’d like to help solve and search opportunities by category on platforms like Idealist and Volunteer Match. You can also spend the time trying a career interest on for size. A significant number of companies are offering virtual internships this summer, and you can search platforms like LinkedIn, internships.com, Handshake, Way Up and Intern From Home for remote opportunities in any field you’re interested in. Just keep in mind that any gap time you take will need to be spent productively and likely in one place. Backpacking across three continents is out in the age of coronavirus, but giving back and building a new skillset are definitely in. Thank you so much for joining me today on HerMoney. Thanks to Maria Konnikova for being with us and sharing her insight on all things related to risk and the chances that we take in life. If you like what you hear, please subscribe to our show at Apple Podcasts. Leave us a review because we love hearing what you think. We want to thank our sponsor Fidelity. We record this podcast out of CDM Sound Studios. Our music is provided by Video Helper. Thank you so much for joining us and we’ll talk soon.